By

By January 2025, Property Market Report for Irlam, Cadishead and Rixton

In this update I will be reviewing how the year has started and the key statistics from January to give the most comprehensive overview of the UK property market.

January 2025 has seen a higher number of properties for sale, an increase in the level of new listings entering the market, and a surge in the volume of sales agreed when compared to both January last year and the six-year average.

The uplift in activity levels has also been matched by average UK house prices rising by £11,778 and 4.24% as of November in comparison to the start of 2024 as reported by the latest data from the land registry.

The average asking price on new listings in January were up by 1.75% on a year ago and 3.44% for properties that have had sales agreed.

The first month of the year tends to give an indication as to how the rest of the year will play out and the statistics for January is really strong evidence that the UK property market is in shape for a very positive 2025.

2025 has started much better off than the previous five years with the exception of the number of sales agreed in January 2021 as demand was heavily fuelled at that time with buyers trying to beat the original Covid stamp duty deadline which was set for the start of April that year before being extended in the March budget. Whilst some buyers will be rushing to beat the stamp duty deadline now, the window for guaranteeing completion before the stamp duty changes come into place is rapidly closing in. In the past, only 29% of sales agreed complete within three months, with that figure falling to 13% within two months, and only 6% complete within a month.

Based on the below data, any market activity in January is arguably from buyers who know the chances of them beating the stamp duty cut off point is very slim and points towards strong demand continuing following the stamp duty changes.

Therefore we should not expect too much of a major impact on activity levels going forward, especially as approx 60% of first time buyers will still pay no stamp duty from April and the extra costs to homeowners remains manageable.

Having navigated higher inflation, interest rates, and house prices in recent years, it has become normal for homemovers to combat increased costs when it comes to moving home.

There has also been a boost to the number of sellers deciding to try their luck at selling again having previously failed to do so and this would appear to promote the fact that these homeowners do not have concerns in the near future of demand dropping off due to the impending stamp duty changes.

What we have also observed in January is a reduced number of sellers lowering their asking prices compared to the start of last year, which would suggest more homeowners are being realistic from the outset and increased buyer confidence is resulting in more sales being agreed closer to the originally set price. However, price reductions are still significantly higher than the six-year average and highlights that there are still some overly optimistic sellers who are needing to adjust their asking prices to attract the cost conscious and value seeking buyers.

The number of properties withdrawing from the market in January was considerably lower than last January and the six-year average, which gives off the impression that there are a lot more serious sellers on the market right now compared to recent years and are much more committed to moving as opposed to those that have perhaps just been chancing their arm to see if they can achieve a crazy price for their property.

I’ve covered off market activity and prices, now for inflation, mortgage approvals, and completed transaction volumes which all have a direct impact on consumer confidence and what happens in the market going forward.

Inflation dropped surprisingly to 2.5% in December and meant the annual average for 2024 ended up at 2.53% compared to 7.37% in 2023 and 9.07% in 2022.

The 10-year average for inflation is 2.98% and it was 4% in December 2023.

The return of inflation to more normal levels has meant the base rate and mortgage rates have come down ever so slightly and this has supported an increase in positive sentiment, market activity, house prices, mortgage approvals and completed transactions.

Completed transactions from the land registry in December were 3.98% higher than November, 19.78% more than December 2023, plus they were 6.49% up on the 12-month average for 2024, but were 4.2% down on the 10-year average for December.

There were 66,500 mortgage approvals in December, a 1.22% increase on November, and a 31.68% jump on December 2023, plus they were 6.24% higher than the 12-month average for 2024, and were only 0.62% lower than the 10-year average for December.

The ‘effective’ interest rate – the actual interest paid – on newly drawn mortgages decreased by 3 basis points, to 4.47% in December, the lowest since April 2023.

The rate on the outstanding stock of mortgages remained broadly unchanged in December at 3.79%.

The average 2-year and 5-year fixed rates also remain pretty much unchanged at 4.98% and 4.77%.

This is the same for the lowest rates for 2-year and 5-year mortgages at 4.15% and 4%.

Barclays and Coventry Building Society announced mortgage rate reductions ahead of the Bank of England’s base rate cut on 6th February. Barclays has also cut rates on some of its mortgages for home buyers and people remortgaging, while also introducing new rates for borrowers purchasing energy efficient homes, with rates starting from 4.13%. In addition, it has also launched a two-year tracker mortgage with a 5.24% with no product fee. Meanwhile, Coventry Building Society has cut its fixed rates by up to 0.27% as well. Halifax also cut rates by up to 0.3% on remortgage deals, while home movers and first-time buyers will see rate reductions of up to 0.11%.

Elsewhere, Clydesdale’s cuts saw a number of its two-year and five-year fixed rate mortgage deals lowered by up to 0.28%, while HSBC’s changes to both its residential and buy-to-let product range Molo Finance has announced rate reductions of 20 basis points on its UK resident two-year and five-year buy-to-let products, effective immediately and Accord Mortgages has announced that, due to market fluctuations, it has made rate cuts across both its buy-to-let and residential product ranges. The changes that have come into effect include reductions of up to 0.10% across a wide selection of residential products from 75% loan-to-value, including products for borrowers with just a 5% deposit.

I must note that whilst there has been marginal increases in mortgage rates in recent weeks, despite some lenders cutting rates across their mortgage products.

The BoE met for the first time in 2025 on 6th February and voted to drop the Bank Rate 25bps to 4.5% and the lowest it has been since June 2023. With seven MPC members voting for this drop and two others voting for even bigger cuts to

4.25%, which was largely anticipated by the financial markets with the market pricing in an 84% chance of this cut happening. This has followed similar reductions in August and November last year, aligning with the MPC approach of ‘gradual’ guidance to reduce the base rate, with financial markets now predicting two/three additional rate cuts this year, bringing the base rate down to below 4%.

However, the surprise pattern of two members voting for cuts to 4.25% certainly does open the door for the potential of more or bigger cuts to the base rate throughout 2025.

We should not get too carried away with this though as whilst it is clear from the lenders above who had cut some of their rates already and shown early signs of wanting to be as competitive in the lending market as they can be because the path of base rates is already priced into fixed-rate mortgages, which account for the majority of new mortgages. Swap rates had been falling in anticipation of the base rate cut with Five-year swap rates down from 4.12% to 3.92%, and two-year swaps from 4.26% to 4.06%.

However, due to where the global financial markets, swap rates and gilt yields currently are, there is no expectation that interest rates will drop much further from where they sit at the moment. UK long-term borrowing costs have hit a 27-year high, the yield on 10-year gilts reached its highest level since 2008, and 30-year gilts were at their highest level since 1998. Whilst there is no expectation of interest rates dropping much further due to the above, the cut to the base rate as evidenced last year, will provide a boost to market sentiment for home buyers, more than a boost to buying power.

House Price Index Update The latest House Price Index reports from the major players has given a 0.25% monthly increase for prices and 2.06% annually, which is a further sign of positivity in the market for house price growth. The January Rightmove House Price Index reported an 11% increase in the number of new properties coming to the market versus the same period last year and saw the average asking price rise by 1.7%, which was the largest jump in prices at the start of the year since 2020. This has resulted in buyers having the highest level of choice at the start of the year in ten years and this increased level of supply has been matched by demand with the level of buyers contacting estate agents 9% higher since Boxing Day compared to the year before.

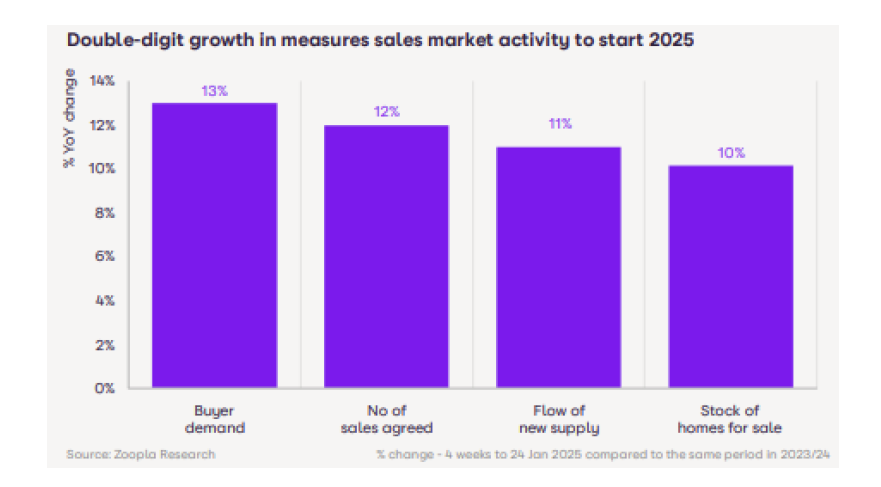

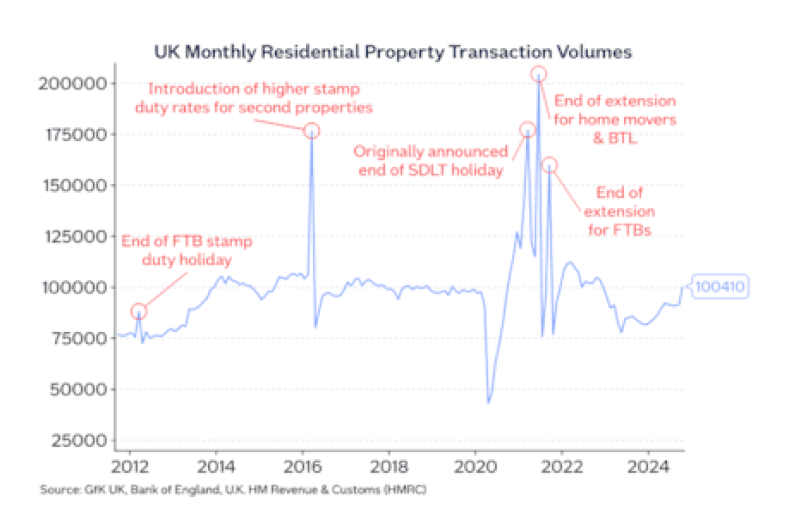

Rightmove also recorded its busiest start to a year for Mortgage In Principle applications, which is further evidence of buyer intent going forward. As you can see from the image above, Zoopla have also shared positive activity in their first House Price Index of the year, reporting buyer demand is 13% higher than a year ago, new listings increased by 11%, with 10% more properties for sale and 12% additional sales agreed. I mentioned earlier on that the latest data is giving the impression that buyer demand is not going to fall off a cliff when the stamp duty changes at the end of March, but you do usually see a spike in completions to beat the deadline and then a softening in transaction numbers following the changes as you can see from the image below.

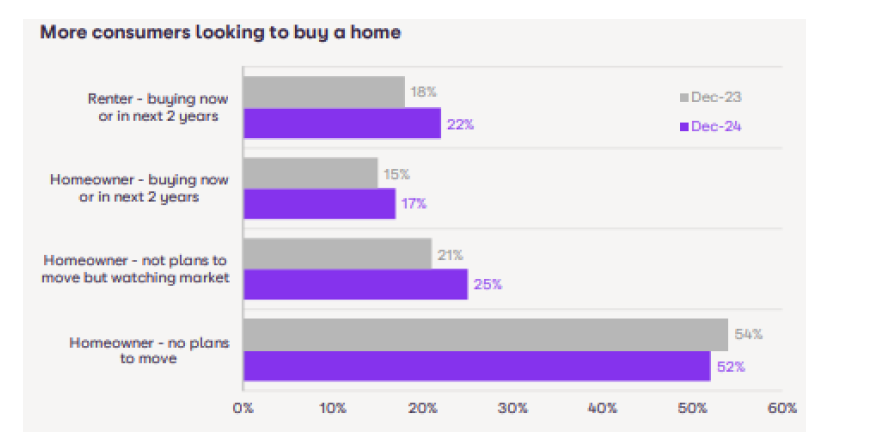

However, the latest Zoopla Monthly Consumer Tracker shows there has been an increase in the number of households wanting to move, with 17% of existing homeowners wanting to move in the next two years and 22% of renters wanting to purchase as well. It is also very interesting to see that whilst 25% of homeowners have no plans to move, they are watching the market and perhaps if affordability does improve or the house of their dreams comes on the market, this might see an increase in the aspirational movers who make up the extra discretionary transactions.

Conclusion

The strong end of year performance and momentum in the property market has most definitely spilled over from 2024 into 2025 with an increase in supply and demand, despite some softening in consumer confidence over the economic outlook. However, consumer confidence is definitely higher than it was a couple of years ago with demand 26% higher than at the start of 2023 according to Zoopla and I think this highlights that whilst there are still challenges with affordability, the market has adjusted to economic challenges.

The UK property market has begun 2025 with cautious optimism and the various statistics from a variety of sources looking at things such as transactions, new listings, properties for sale, sales agreed, and mortgage approvals is indicating a positive outlook for the rest of the year. Thank you for reading my January 2025 market update and I do hope you have found the insights valuable.

Cadishead Market Update – January 2025

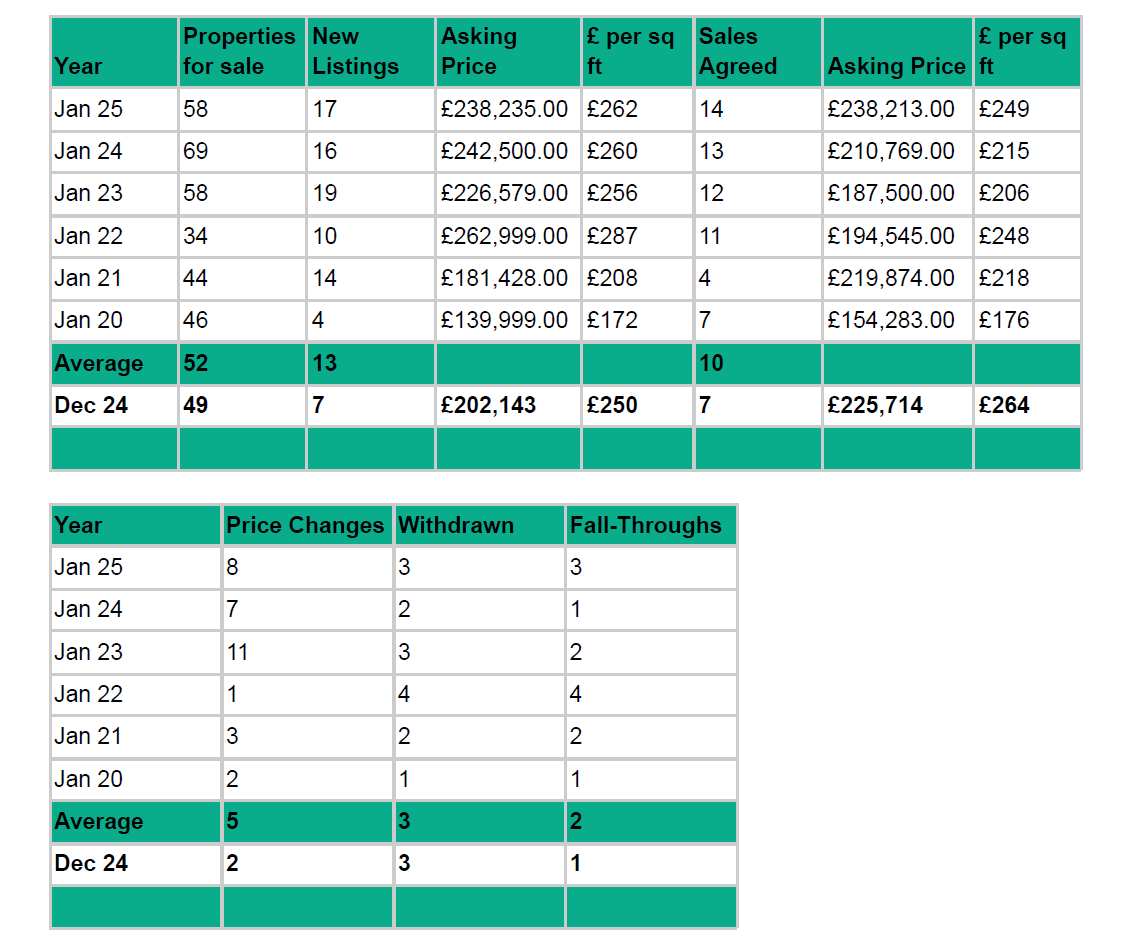

The Cadishead property market is off to a flying start in 2025! There are 58 properties for sale, slightly above the six-year average of 52. New listings have also been busy, with 17 hitting the market in January—outpacing the usual 13. Clearly, plenty of homeowners have put “sell the house” at the top of their New Year’s resolutions!

The average asking price sits at £238,235, which works out to £262 per square foot. Over to sales agreed—January saw 14 properties snapped up, exceeding the usual 10, with an average asking price of £238,213 (£249 per square foot).

Elsewhere in the market, there were 8 price corrections (up from the usual 5), 3 withdrawn properties (on par with the average), and 3 fall-throughs, slightly above the norm of 2.

Conclusion: Cadishead’s market has had a busy and energetic start to the year! More listings, more sales, and only a few bumps along the way. It’s shaping up to be a competitive market, so buyers need to be quick, and sellers—well, pricing it right is still key!

Irlam Market Update – January 2025

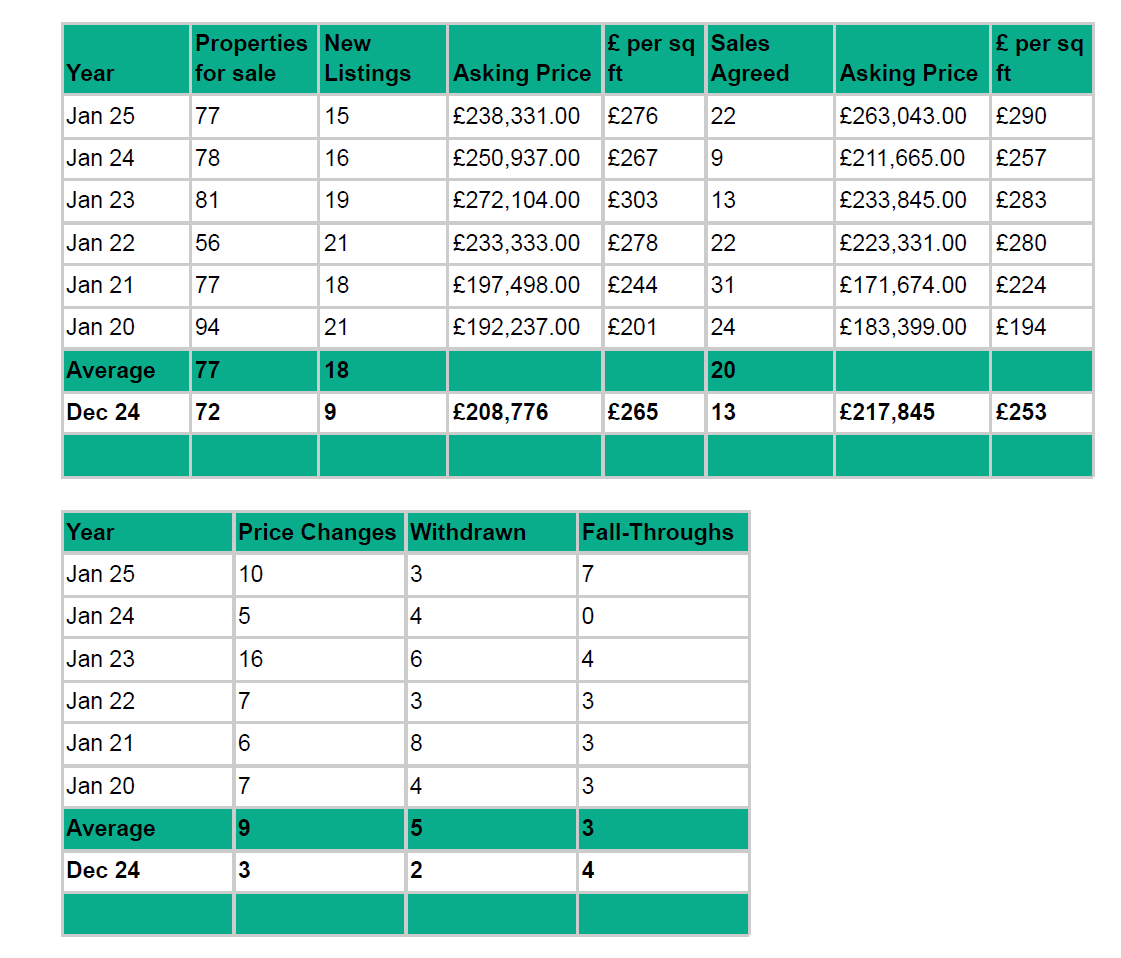

Irlam is holding steady, with 77 properties for sale, exactly in line with the six-year average—clearly, Irlam doesn’t do unpredictability! New listings were a touch lower at 15, compared to the usual 18, suggesting some sellers are still shaking off the post-Christmas slump.

The average asking price is £238,331, equating to £276 per square foot. Over on the sales side, January was a strong month, with 22 properties agreed, slightly above the six-year average of 20. The average asking price for these was £263,043, working out at £290 per square foot.

In other market activity, 10 price corrections were made (just above the six-year average of 9), while 3 properties were withdrawn (compared to the average of 5). However, 7 sales fell through, which is higher than the usual 3—perhaps some buyers got cold feet or just spent too much at the January sales!

Conclusion: Irlam’s property market is ticking along nicely—more sales than usual, stable asking prices, and just a few wobbles with fall-throughs. Buyers are still out in force, so if you’re selling, now’s a great time to make sure your home stands out!

Rixton and Lowton Market Update – January 2025

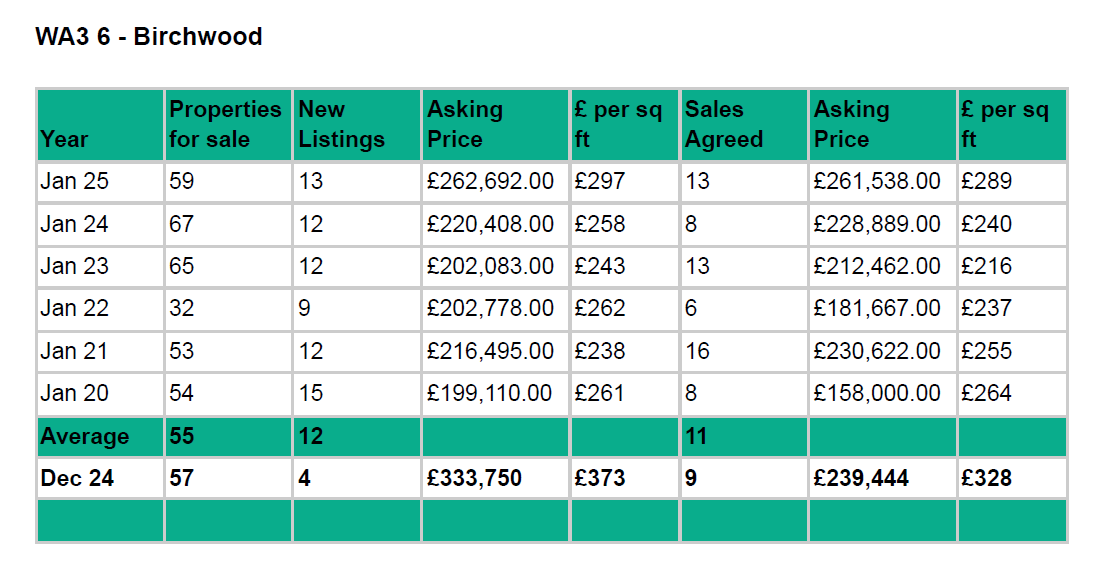

The WA3 6 postcode is keeping estate agents on their toes! There are 59 properties for sale, with 13 new listings added in January. The average asking price for these was £262,692, equating to £297 per square foot.

Sales activity has been strong, with 13 properties going under offer, ahead of the six-year average of 11. The average asking price for agreed sales was £261,538, working out to £289 per square foot.

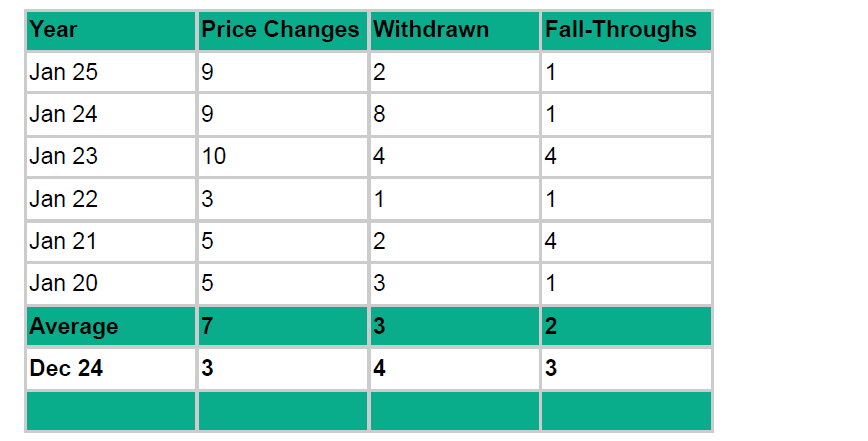

Elsewhere, there were 9 price reductions (up from the average of 7), 2 withdrawn properties (below the usual 3), and just 1 fall-through, compared to the six-year average of 2—so, not too many broken hearts this month!

Conclusion: The WA3 6 market is showing resilience, with solid sales and only a handful of price adjustments. With demand still strong, now’s a great time for sellers to take advantage—just make sure that price is right to attract those eager buyers!

- Cadishead property market

- Irlam house prices

- WA3 6 property update

- January 2025 property market

- Houses for sale in Cadishead

- Estate agents in Irlam

- Local property trends

- Property price corrections

- Homes for sale in WA3 6

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link