By

By Bank of England Cuts Base Rate Again — Now at 4%

📅 August 7, 2025

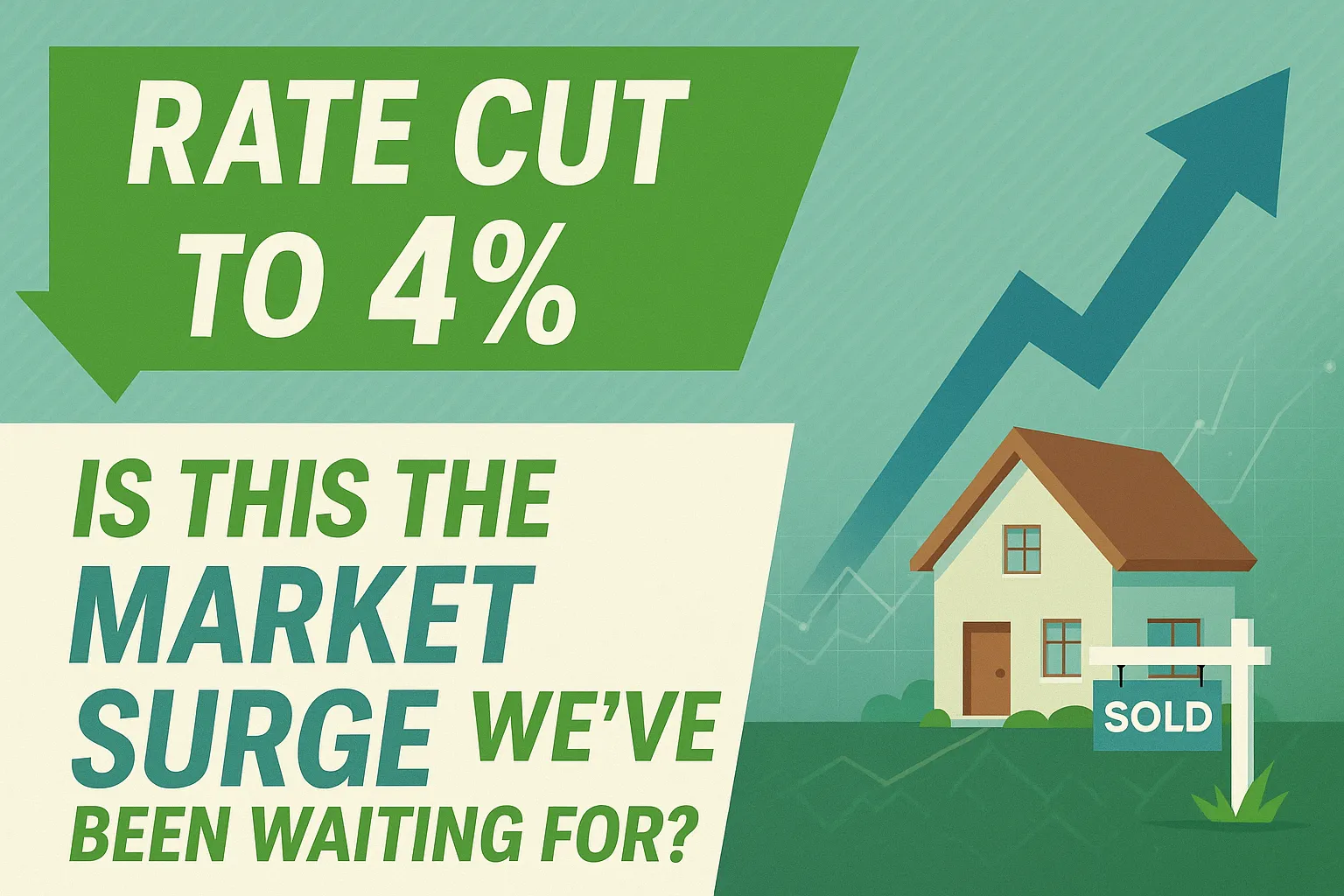

Just three months after trimming the base rate to 4.25%, the Bank of England has announced a further cut to 4%, signalling a continued shift toward easing borrowing costs and restoring long-term economic stability.

This marks the fifth rate reduction since August 2024, with the Bank gradually reversing the sharp hikes we saw during the inflation crisis of 2022–2023. The current rate is now at its lowest point since early 2023.

Why Another Cut?

The latest decision was driven by encouraging economic data:

Inflation is continuing to ease, staying close to the 2% target despite temporary spikes in energy prices.

Consumer confidence is on the rise, with spending, saving, and mortgage activity stabilising.

Global markets have shown greater resilience, despite ongoing trade uncertainties.

The Bank’s Monetary Policy Committee (MPC) voted 6–3 in favour of the reduction, reflecting increased consensus on the need to support households and businesses as recovery momentum builds.

What This Means for the Property Market

The positive effects of rate cuts are already being felt across the UK housing market, and this latest reduction will likely amplify that trend:

✅ More Affordable Mortgages

With base rates now at 4%, fixed-rate mortgages have continued their downward trajectory. Many mainstream lenders are now offering sub-4% deals, particularly on 2- and 5-year fixed products.

This translates to:

Lower monthly payments for new buyers.

Cheaper remortgage options for those coming off fixed deals.

Greater borrowing power for movers and first-time buyers.

✅ Increased Buyer Demand

Each rate cut has seen an uplift in activity:

More Rightmove views

Higher levels of enquiries

More viewings booked

Stronger attendance at open houses

Estate agents across the UK (including us at Oliver James Estate Agent) are reporting heightened interest from first-time buyers and investors, especially those previously priced out by high mortgage stress tests.

✅ Market Confidence Returning

Consumer confidence around buying, selling, and remortgaging has been growing steadily since the first rate reduction in August 2024. With five cuts now completed, buyers and sellers are beginning to feel the worst may be behind us.

This increased certainty means more people are taking action, especially ahead of any potential changes in government policy or global economic shifts.

What Sellers Should Know

If you're considering selling, now could be one of the best windows to make your move:

Buyers have more confidence and greater affordability.

New listings have increased, but competition remains manageable.

Well-presented homes are achieving strong prices in short timescales.

As interest rates fall, more buyers are entering the market – and that surge in demand creates a fantastic opportunity for sellers.

What’s Next?

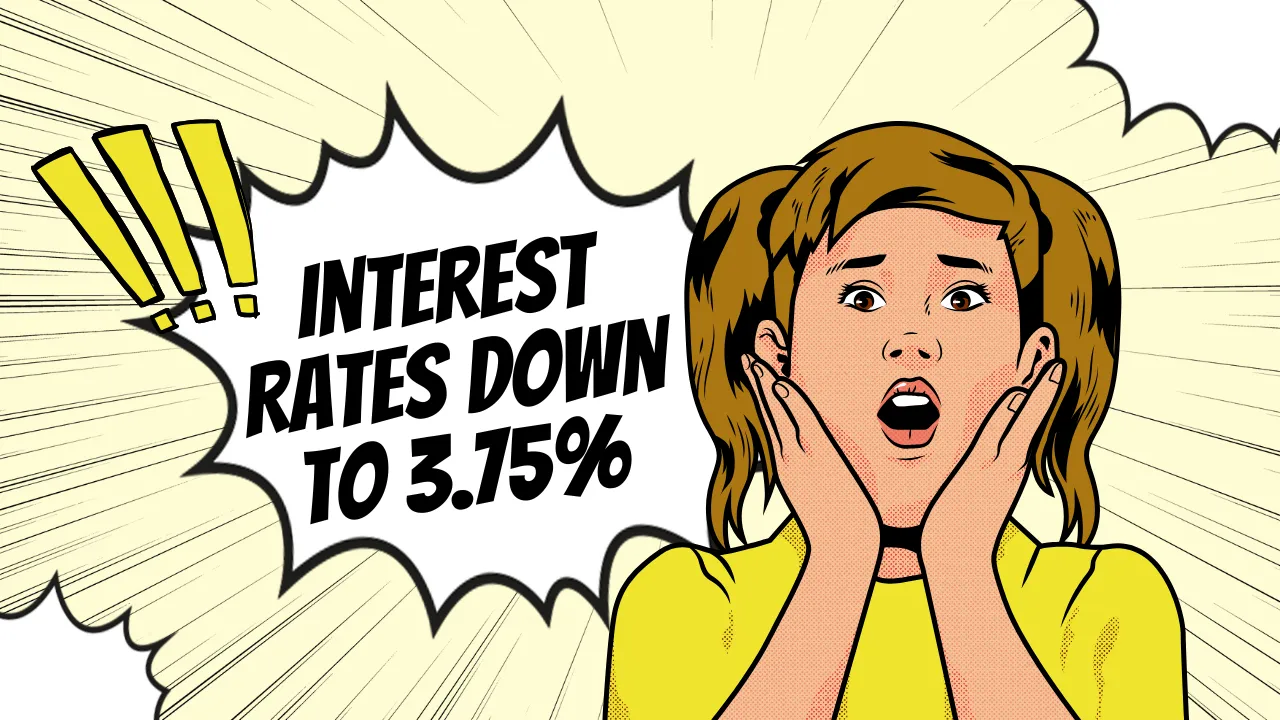

While no one can predict the exact path of interest rates, the Bank of England has signalled a careful and data-driven approach going forward. Further cuts are possible if inflation remains stable.

Financial markets are currently pricing in the possibility of another cut by the end of 2025, potentially taking the base rate to 3.75%.

Final Thoughts

After years of uncertainty, we’re finally seeing green shoots in the UK housing market. The rate cuts to 4.25% in May and now 4% in August represent a meaningful step toward recovery.

If you’re thinking about moving, remortgaging, or simply curious about your home’s value in the current climate, now is a brilliant time to explore your options.

📲 Get a touch for a free valuation.

Bank of England base rate 2025

Interest rate cut UK August 2025

Mortgage rates after base rate cut

Should I sell my house now UK

Buyer demand UK property market

Effect of interest rate cut on housing market

UK property forecast 2025

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link